How to Cash Out Crypto for Your Business

So, you've accepted crypto and now it's time to turn that digital currency into cold, hard cash. For most businesses, the simplest and most well-trodden path is through a major centralized exchange (CEX) like Kraken or Coinbase. The process is pretty straightforward: you send the crypto from your business wallet to the exchange, sell it for your local currency, and then transfer the funds directly to your business bank account.

A Merchant's Quick Guide to Cashing Out Crypto

As a merchant or developer, figuring out how to efficiently convert your crypto into usable cash is a crucial part of your operations. Your best strategy will boil down to four things: speed, fees, security, and the size of the transaction. Cashing out a small payment from a customer has entirely different requirements than liquidating a six-figure revenue stream.

While the crypto world is always changing, centralized exchanges like Binance, Coinbase, and Kraken are still the go-to for most businesses. They handle the lion's share of all crypto-to-fiat conversions for a reason—their process is reliable. You deposit your coins, trade them for USD or EUR, and pull the money out. Depending on your bank and the withdrawal method you pick, you could see the funds in a few hours or a few days.

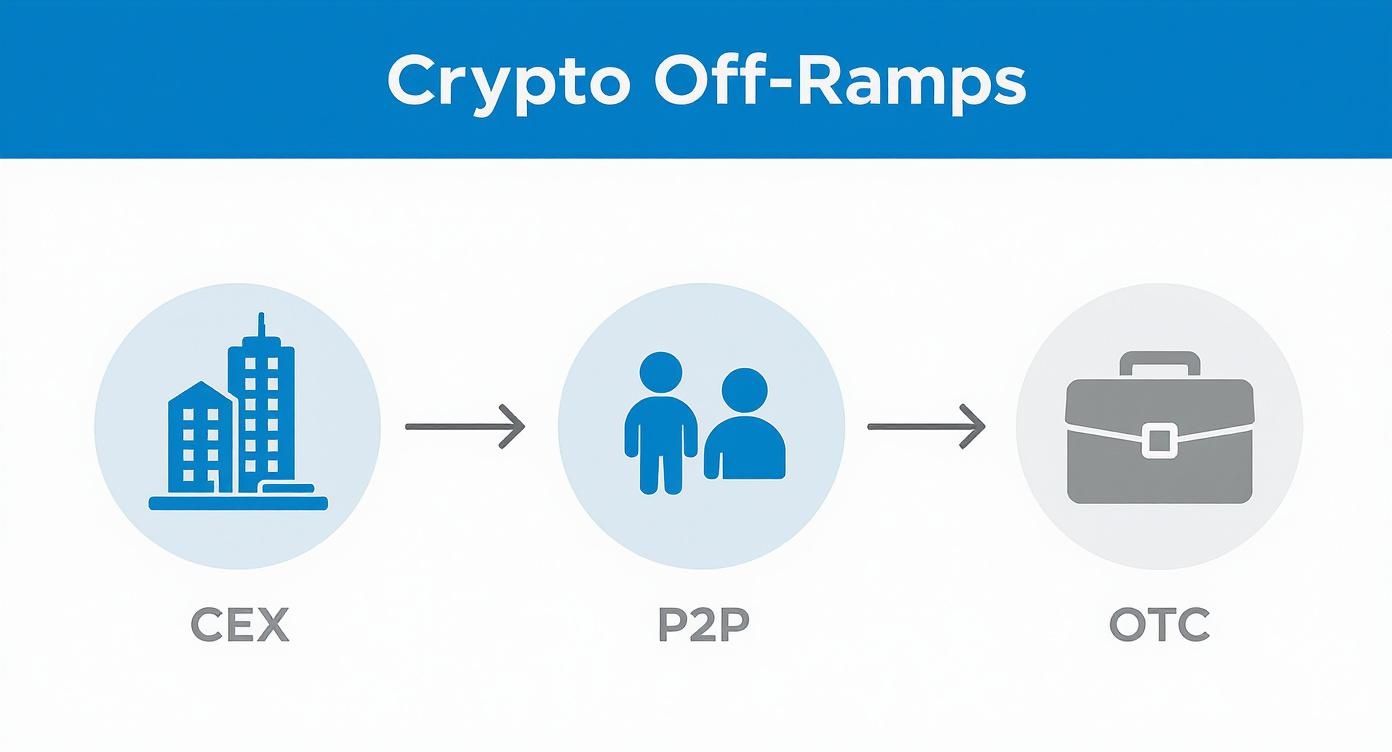

Crypto Cash-Out Methods at a Glance

To make the right call, it helps to see your options laid out clearly. Each method is built for a different purpose, whether you need instant spending power for small amounts or a secure way to handle massive trades.

| Method | Best For | Typical Speed | Fee Structure |

|---|---|---|---|

| Centralized Exchange (CEX) | Most businesses; small to medium volumes | 1-5 business days | Trading fees + withdrawal fees |

| Peer-to-Peer (P2P) | Regions with limited banking; flexibility | Varies (minutes to days) | Low to no platform fees |

| Over-The-Counter (OTC) | Large volumes ($100k+); institutional | 1-3 business days | Negotiated fixed percentage |

| Crypto Debit Card | Instant spending; small, daily use | Instant | Reloading and transaction fees |

This table should give you a solid starting point. A CEX is a safe bet for most day-to-day business transactions because it operates in a regulated and dependable environment. P2P platforms give you more direct control, but they also carry risks that mean you have to be extra careful about who you're dealing with.

Key Takeaway: For any business needing to liquidate a large amount of crypto, an OTC desk is almost always the best option. It helps you avoid "slippage"—where your own large sell order actually pushes the market price down—and locks in a predictable exchange rate for the entire amount.

Finally, don't forget the paperwork. Managing these crypto-to-cash transactions means keeping meticulous records. It's just as important to have a firm grasp on traditional accounting practices, including understanding what an invoice is and how it fits into your financial workflow. Proper invoicing ensures every dollar (or satoshi) is accounted for, which is non-negotiable for clean books and staying on the right side of the tax authorities.

Choosing the Right Way to Cash Out Your Crypto

Figuring out the best way to turn your crypto into cash isn't a one-size-fits-all deal. It's really about matching the right tool to your specific situation. A small online shop cashing out a few hundred dollars a day has completely different needs than a dev agency that just got paid six figures in crypto for a big project.

Your choice—whether it's a mainstream exchange, a peer-to-peer platform, or a private OTC desk—will directly impact your fees, your security, and how quickly you can get your hands on your money.

Your Go-To Option: The Centralized Exchange

For most businesses, the first stop is a Centralized Exchange (CEX). Think of giants like Kraken, Coinbase, or Binance. They're the default for a reason. These platforms have deep liquidity, which means you can sell a decent amount of crypto without sending the price tumbling. Their interfaces are usually pretty straightforward, making it simple to deposit crypto, trade it for dollars or euros, and send the cash to your bank.

But that convenience comes with a catch. The biggest one is custodial risk. When your crypto is sitting on an exchange, you’re trusting them to keep it safe. While the big players have solid security, they are a massive target for hackers. On top of that, businesses often smack into withdrawal limits, which are tied to how much Know Your Business (KYB) verification you’ve completed. Bumping up against a daily or monthly limit can throw a real wrench in your cash flow.

A CEX is probably your best bet if you're dealing with:

- Regular, moderate-volume sales: Perfect for cashing out daily or weekly revenue that’s comfortably under the withdrawal caps.

- A need for speed: For typical amounts, it’s usually the fastest way to get money from your crypto wallet to your business bank account.

- A team that likes a familiar feel: The experience is a lot like using a traditional online banking portal, which keeps the learning curve low.

The Direct Route: Peer-to-Peer (P2P) Platforms

If you move away from the big exchanges, you’ll find Peer-to-Peer (P2P) platforms. These operate more like a Craigslist or eBay for crypto, connecting buyers and sellers directly. For businesses in countries with tricky banking systems or strict rules on moving money, P2P can be an absolute game-changer. It opens up all sorts of payment methods, like local bank transfers or even mobile money.

The main draw here is the potential for better exchange rates and lower fees since you’re cutting out the middleman. But with that flexibility comes a much higher degree of risk. Scams are a real and constant problem on P2P marketplaces, from fake payment confirmations to outright theft. You absolutely have to do your homework on who you’re trading with and always, always use an escrow service.

A Word of Warning from Experience: Fraud is no joke in the P2P world. I can't stress this enough: always use the platform's escrow service. Never release your crypto until you have visually confirmed the money is cleared and settled in your bank account. A moment of impatience can cost you everything, and there's no "undo" button.

When You're Moving Serious Volume: OTC Desks

So, what do you do when you need to cash out a sum that would make the market sneeze on a regular exchange—say, $100,000 or more? This is where Over-The-Counter (OTC) desks come in. These are specialized services, often run by the big exchanges or dedicated brokerage firms, that handle large, private trades.

Instead of placing a massive sell order on the public market—which would set off all sorts of alarms and cause price slippage—an OTC desk quietly finds a buyer for your entire block of crypto. They give you a single, locked-in price for the whole deal. This "white-glove" service means you get a predictable amount of cash, and you don’t torpedo the market price in the process.

Let's walk through a real-world example. Imagine a software firm lands a $250,000 project and gets paid in ETH. If they tried to sell all that ETH on Coinbase at once, their own sale would push the price down. The first chunk might sell at a good price, but the last chunk would sell for much less. By using an OTC desk, they get a single quote for the entire $250,000 worth of ETH. They know exactly how much cash they'll receive, minus a small, agreed-upon fee. For any business handling serious crypto revenue, that kind of price stability is not just a luxury—it's essential.

Automating Crypto Payouts with an API

If your business accepts crypto, you know the drill. Manually cashing out payments is a massive time sink. Logging into an exchange, making the trade, and then withdrawing the funds for every single transaction just doesn't scale. It quickly becomes a serious operational headache.

This is where a payment API comes in. Think of an API (Application Programming Interface) as a secure messenger that lets your business systems talk directly to a crypto payment provider. Instead of you doing the work by hand, you can set up automated rules to manage your crypto revenue programmatically. It’s a game-changer for turning a tedious chore into a smooth part of your cash flow.

Building Your Automated Off-Ramp

Integrating an API from a provider like BlockBee lets you set the rules of the game for your payouts. You stop reacting to individual payments and start proactively managing your funds based on logic that you define. For any growing business, this is a much smarter way to handle crypto.

This approach puts developers in the driver's seat, allowing them to build a custom, automated off-ramp perfectly suited to their needs.

- Programmatic Conversions: You can set up a rule to instantly convert incoming crypto like Bitcoin or Ethereum into a stablecoin like USDT or USDC. This is a brilliant way to lock in the value of your revenue and sidestep price volatility.

- Threshold-Based Payouts: Why cash out every small payment? Set a rule to trigger a payout only when your balance hits a certain amount. For example, you could automatically cash out every time you accumulate $5,000 in crypto, which means fewer, larger transactions and lower overall fees.

- Batched Transactions: Another great trick is to bundle many small payments into one big payout. This makes life so much easier for your accounting team, who now have to track one line item instead of dozens.

This infographic breaks down the different routes your crypto can take on its way to becoming fiat—all of which can be automated with a solid API.

The real takeaway is that automation gives you a central control panel. You can decide whether to use an exchange, a P2P service, or an OTC desk for your off-ramp, all based on the business rules you’ve put in place.

A Practical Scenario for an E-commerce Store

Let's say you run an online store that gets dozens of small crypto payments every day. Cashing those out one by one would be a complete nightmare.

With an API, you could create a workflow that automatically sweeps all those daily payments into a single wallet. At the end of the day, a script could convert the total balance into a stablecoin. Then, once a week, another trigger sends that stablecoin balance as a single payout to your business bank account. The entire process hums along in the background with zero manual effort. You get predictable cash flow without the daily grind.

You can learn more about how platforms like BlockBee make automated payouts available for all users and see how the nuts and bolts fit together.

Expert Insight: The real power of an API isn't just automation; it's control. You can build sophisticated logic that responds to market conditions, such as pausing conversions during extreme volatility or accelerating payouts when a certain price target is hit. This elevates your crypto treasury management from a simple administrative task to a strategic financial function.

This level of automation does more than just save time. It slashes the risk of human error, tightens security by reducing manual access to funds, and creates a clean, auditable trail for every transaction. For any merchant serious about scaling their crypto operations, a payouts API isn't a nice-to-have—it's essential.

Managing Security and Compliance Risks

Learning how to cash out crypto is a lot more involved than just hitting a "sell" button. Every time you turn digital assets into fiat, you’re conducting a major financial transaction. This comes with some serious security and compliance responsibilities.

Ignoring these is like leaving the vault door wide open. You're exposing your business to all sorts of risks, from outright theft to painful regulatory penalties. It’s crucial to treat your crypto off-ramp with the same discipline as your core banking operations.

Fortifying Your Funds Against Threats

Your first line of defense is always going to be solid security. The digital world is full of bad actors looking for an easy score, so your protective measures have to be rock-solid, especially when you're moving funds to convert them.

A great place to start is by segregating your funds. Your business should never keep its entire operational balance on a centralized exchange—that’s just asking for trouble. Instead, keep the majority of your crypto assets in a hardware wallet (often called cold storage) and only move what you plan to cash out.

From there, get serious about who can access your accounts.

- Multi-Factor Authentication (MFA): This is completely non-negotiable. Use an authenticator app like Google Authenticator or, even better, a physical security key like a YubiKey for every account. SMS-based 2FA is a last resort; it’s too vulnerable to SIM-swapping attacks.

- Address Whitelisting: This is a fantastic feature offered by most good exchanges. It lets you pre-approve a list of specific withdrawal addresses. That way, even if a hacker somehow gets into your account, they can only send funds to wallets you already own and control.

These steps aren't just checkboxes; they create a layered defense that makes it exponentially harder for anyone to get their hands on your funds.

Key Takeaway: Think of your crypto security in layers. A hardware wallet is your main vault, MFA is the guard at the door, and address whitelisting is the only approved route for the armored truck. Each layer makes a potential breach that much more difficult.

Navigating the World of Crypto Compliance

Beyond just keeping your assets safe, you have to play by the rules. The world of finance is a regulated one, and crypto is no exception. Exchanges and OTC desks are legally required to perform due diligence to prevent money laundering and other illicit activities. This is where Know Your Customer (KYC) and Anti-Money Laundering (AML) checks come in.

For businesses, the process is often called Know Your Business (KYB). You’ll need to provide documents that prove your company's identity, who owns it, and where it’s legally registered. It can feel like a bit of a bureaucratic headache, but these checks are what protect the integrity of the whole system—and your business’s reputation along with it. We dive deeper into this in our guide on the role of KYC in crypto.

Don't wait until you need the cash to get this done. Failing to comply can lead to frozen accounts and locked funds, which could bring your entire operation to a screeching halt. Get fully verified with your chosen off-ramp well in advance.

To stay on top of this, many smart businesses are now focused on building a modern compliance risk management framework that puts their crypto procedures in writing. This proactive approach means you’re always ready for regulatory questions and can operate with confidence. In the end, a strong compliance game is the mark of a professional, trustworthy business.

Understanding Your Crypto Tax Obligations

Figuring out how to cash out your crypto is a huge step, but it’s really only half the job. The other, often-ignored half is dealing with the taxes that come along with it. Trust me, overlooking this part can create some serious financial and legal headaches down the road—a costly mistake I’ve seen too many businesses make.

https://www.youtube.com/embed/MNeyYLd7BSI

First things first, you need to understand how the government sees your crypto. In most places, like the United States, cryptocurrencies are treated as property, not currency. This distinction is everything. It means that every single time you sell crypto for cash, you’re creating a taxable event.

Short-Term vs. Long-Term Capital Gains

When you sell crypto for more than you paid, that profit is subject to capital gains tax. The rate you pay hinges entirely on one thing: how long you held the asset before selling. This splits your tax situation into two very different buckets.

- Short-Term Capital Gains: If you held a crypto asset for a year or less before cashing out, any profit is a short-term gain. These gains get taxed at your ordinary income tax rate, the same as your regular business profits, which can be punishingly high.

- Long-Term Capital Gains: Hold that same asset for more than one year, and the profit is considered a long-term gain. These are taxed at a much lower, more favorable rate. For many businesses, this can translate into significant tax savings.

This difference gives you a massive incentive to think strategically about your holding periods, especially for larger crypto positions you don't need for immediate operational expenses.

Calculating Your Taxable Gain

So, how do you figure out what you owe? The formula itself is simple: Sale Price - Cost Basis = Capital Gain (or Loss).

Your cost basis is just the total amount you spent to get the crypto in the first place, including the purchase price and any transaction fees. For example, if your business bought 1 ETH for $3,000 and paid a $50 fee, your cost basis is $3,050. If you later sell that ETH for $4,000, your taxable capital gain is $950.

That’s easy enough for one transaction. But what happens when you’re dealing with hundreds of crypto payments from customers, all received at different times and at different prices? It gets complicated, fast.

A Non-Negotiable Reality: You absolutely must keep flawless records. For every single transaction, both incoming and outgoing, you need to log the date, the fiat value at that exact moment, the amount of crypto, and any fees. Without this data, calculating your tax liability accurately is a complete non-starter.

Your Best Allies: Tools and Professionals

Trying to track every transaction manually in a spreadsheet is, frankly, a recipe for disaster. The sheer volume of data is overwhelming, and it’s all too easy to make a costly error. This is where specialized crypto tax software isn't just a nice-to-have; it's essential.

Platforms like Koinly, CoinTracker, or ZenLedger are lifesavers. They can sync directly with your wallets and exchange accounts, automatically pull in your transaction history, and calculate your cost basis using accepted accounting methods (like FIFO or HIFO). They then generate the specific tax forms you need, saving you countless hours and dramatically cutting down the risk of mistakes.

But even the best software can’t replace a real human expert. The tax code is a beast, and crypto regulations are always in flux. Sitting down with a qualified tax professional who genuinely understands digital assets is non-negotiable. They can guide you through the gray areas, ensure you’re 100% compliant, and help you build a tax strategy that actually supports your business goals. Remember, good record-keeping is the foundation of financial clarity; our guide on what is payment reconciliation explains why this is so critical.

Common Questions About Casing Out Crypto

Even with a solid plan, the process of turning crypto into cash can feel like navigating a maze. For businesses and developers, getting clear, practical answers is crucial for building a reliable off-ramp. Let's tackle some of the most common questions that pop up.

What’s the Fastest Way to Cash Out Crypto?

When you need cash in your bank account now, your best bet is almost always a major centralized exchange (CEX) where your business is already fully verified. If you’ve got a business account set up and linked to your bank, that’s your express lane.

Some exchanges will even let you withdraw instantly to a debit card, but watch out—you'll pay a hefty premium for that convenience. Geography also plays a huge role. A SEPA transfer in Europe can land in your account in a matter of hours, whereas a standard ACH transfer in the U.S. will likely take 1-3 business days.

My Two Cents: For any business, "fastest" isn't just about raw transaction speed. It's about finding the sweet spot between speed, reasonable fees, and security. Rushing the process and skipping your security checks is just asking for trouble.

Are There Limits on How Much Crypto I Can Cash Out?

Absolutely. You'll run into withdrawal limits on pretty much every platform out there. These aren't just random numbers; they’re tied directly to how much the platform knows about you. A basic, unverified account will have very tight restrictions, but a fully verified business account will give you much more breathing room.

- Verification Tiers: Exchanges use KYC (Know Your Customer) and KYB (Know Your Business) checks to sort accounts into different levels. The more paperwork you provide, the higher your limits go.

- Daily vs. Monthly Limits: Don’t get caught off guard. Always check both the daily and monthly caps. It’s easy to hit a monthly limit even if your daily withdrawals seem fine.

If you're dealing with a truly large amount—think six figures or more—don't even bother with the regular exchange interface. You need an Over-The-Counter (OTC) desk. They’re built specifically for these high-volume trades and can handle sums that are impossible on a CEX, all without tanking the market price.

How Can My Business Minimize Fees When Cashing Out?

Fees are the silent profit killer if you’re not paying attention. Keeping them low requires a bit of strategy. First off, get in the habit of comparing the fee structures of different exchanges. Don’t just glance at the withdrawal fees; the trading fees are just as important.

A simple but powerful tip: always use the "pro" or "advanced" trading view. These interfaces almost always have a maker-taker fee model, which is dramatically cheaper than hitting the simple "convert" button on the main dashboard.

Another smart move is to batch your transactions. Instead of cashing out every small payment as it comes in, group them together into one larger withdrawal. This single move can slash the impact of fixed, per-transaction fees. And remember, for big amounts, an OTC desk’s ability to prevent slippage will often save you far more than you'd ever pay in CEX trading fees.

Does My Business Pay Taxes Every Time We Cash Out?

In most places, including the United States, the answer is a firm yes. When you sell crypto for fiat currency, it's treated as a disposal of property, making it a taxable event. Your business is on the hook for capital gains tax on any profit you realize from that sale.

How much you owe comes down to your cost basis (what you paid for the crypto) and how long you held it. Meticulous record-keeping isn't just a good idea—it's essential for calculating your taxes correctly. Given how complex and ever-changing crypto tax laws are, working with a tax professional who specializes in digital assets is one of the smartest investments a business can make to stay compliant.

Ready to stop manually managing your crypto revenue and start automating your cash flow? BlockBee provides a powerful, non-custodial API that lets you build a seamless payout system tailored to your business needs. Take control of your funds, minimize fees, and scale with confidence by visiting https://blockbee.io to learn more.